Revenue recognition rules have always played a major role in how businesses report financial performance, but few shifts have been as significant as the introduction of ASC 606. Designed to bring consistency and clarity to how companies recognize revenue, ASC 606 fundamentally reshaped financial reporting across industries, from SaaS and technology to manufacturing and professional services.

But while most discussions focus on revenue reporting, one of the most practical and often misunderstood impacts of ASC 606 falls on sales compensation. Commissions, bonuses, incentives, and contract related expenses are all affected, creating new requirements for tracking, timing, and accounting.

If your organization relies on sales driven revenue, understanding ASC 606 is essential, not just for finance teams but also for sales, RevOps, and leadership. Let’s break down what ASC 606 is, why it exists, and how it affects your sales compensation strategy.

What Is ASC 606?

ASC 606 is a revenue recognition standard issued by the Financial Accounting Standards Board (FASB). The goal is simple: create a unified approach for recognizing revenue across industries and contractual arrangements.

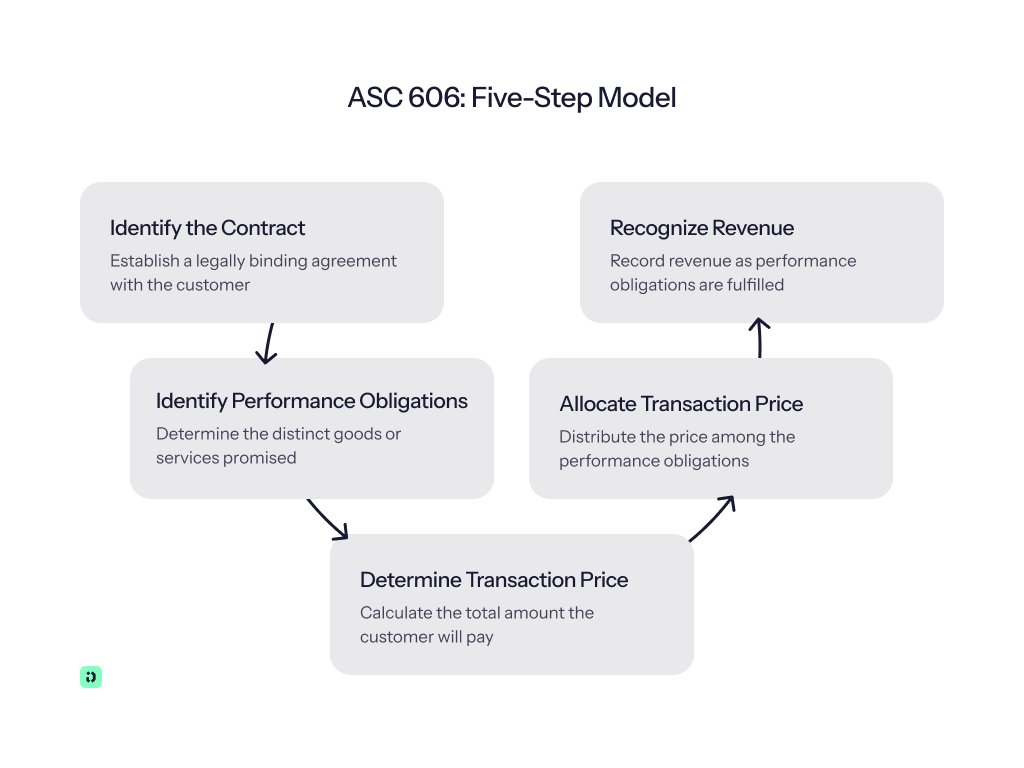

At its core, ASC 606 is built on a five-step model:

1. Identify the contract with the customer

The first step in ASC 606 is determining whether a valid contract exists. A contract is an agreement between a company and a customer that creates enforceable rights and obligations. This step ensures that both parties have approved the arrangement, understand their commitments, and have reasonable expectations of payment and service delivery.

2. Identify the performance obligations within the contract

A performance obligation is any distinct good or service a company promises to deliver to the customer. In this step, the contract is analyzed to identify each separate deliverable. For example, a software subscription, implementation services, and ongoing support may each be considered separate obligations if they provide distinct value.

3. Determine the transaction price

The transaction price is the total amount the company expects to receive in exchange for fulfilling the contract. This amount may be fixed, variable, or a combination of both. Factors such as discounts, refunds, incentives, or variable usage fees must be considered to determine the most accurate estimate of what the company will ultimately earn.

4. Allocate the transaction price to the performance obligations

Once the performance obligations and transaction price are established, the company must assign portions of the transaction price to each obligation. This is done based on their standalone selling prices. Allocating revenue in this way ensures that earnings are tied to the specific goods or services being delivered.

5. Recognize revenue as performance obligations are satisfied

Revenue is recognized when the company fulfills each performance obligation, either over time or at a point in time, depending on the nature of the deliverable. This step ensures revenue is reported in alignment with actual delivery of value, creating consistency and accuracy in financial reporting.This model ensures that revenue recognition aligns with the actual value delivered to customers, not necessarily when the contract is signed or payment is collected.

Why Was ASC 606 Introduced?

Before ASC 606, revenue recognition rules varied widely across industries. Software companies followed one set of rules, manufacturing another, and telecommunications yet another. This created inconsistencies that:

Made it difficult for investors to compare companies

Led to discrepancies in contract interpretation

Allowed organizations to structure contracts to recognize revenue earlier or later

ASC 606 introduced a single, principles based model to standardize revenue reporting, improve transparency, and enhance comparability across businesses.

Sales Compensation Tools and ASC 606 Compliance

Managing ASC 606 requirements becomes dramatically easier when your commission data, calculations, and amortization schedules all live in one place. That’s why many organizations turn to modern sales compensation platforms like Driven.

Driven includes a dedicated ASC 606 compliance module, allowing companies to:

Automatically capitalize and amortize commissions

Maintain audit-ready schedules and documentation

Sync commission data directly with revenue workflows

Track contract changes, renewals, and expansions without manual work

Since all commission data is stored and processed inside the platform, maintaining ASC 606 compliance becomes effortless; no more spreadsheets, manual calculations, or compliance risks.

How ASC 606 Impacts Sales Compensation

While ASC 606 focuses on revenue, it also significantly affects how companies account for commissions and sales incentives, especially those tied to multi, year or subscription, based contracts.

1. Timing of Commission Expense Recognition Has Changed

Under old accounting rules, many companies expensed commissions immediately once paid. ASC 606 changes that.

Now, commissions must be capitalized and deducted over the period the underlying contract provides benefit.

In practical terms:

If you pay a commission for a 3 year contract, you can’t expense it all at once.

You must spread that expense over 36 months, even if the cash is paid upfront.

This aligns expense recognition with revenue recognition.

With ASC 606, the structure of your sales compensation plan determines how commissions are treated:

Compensation Type

ASC 606 Treatment

Upfront Commission for Ongoing Contracts

Capitalize and amortize over contract term

Monthly Commissions

Expense monthly (no amortization)

Renewal Commissions

Capitalize only if they are incremental and expected to provide benefit

Tiered or bonus based Incentives

Must evaluate intent and linkage to performance obligations

A poorly designed plan can create unnecessary accounting complexity or even noncompliance.

3. Increased Documentation and Tracking Requirements

ASC 606 requires companies to track:

Contract assets

Amortization schedules

Commission capitalizations

Adjustments for contract changes

Churn and customer upgrades

Contract modifications

For organizations with large sales teams or variable compensation, this becomes extremely complex without automation.

4. Impacts on Policy, Workflow, and Internal Alignment

Because of the new rules, many companies must revisit:

Sales compensation plans

Finance and accounting procedures

Sales operations and RevOps processes

System integrations between CRM, ERP, and commission tools

ASC 606 forces Sales and Finance to collaborate more closely than ever.

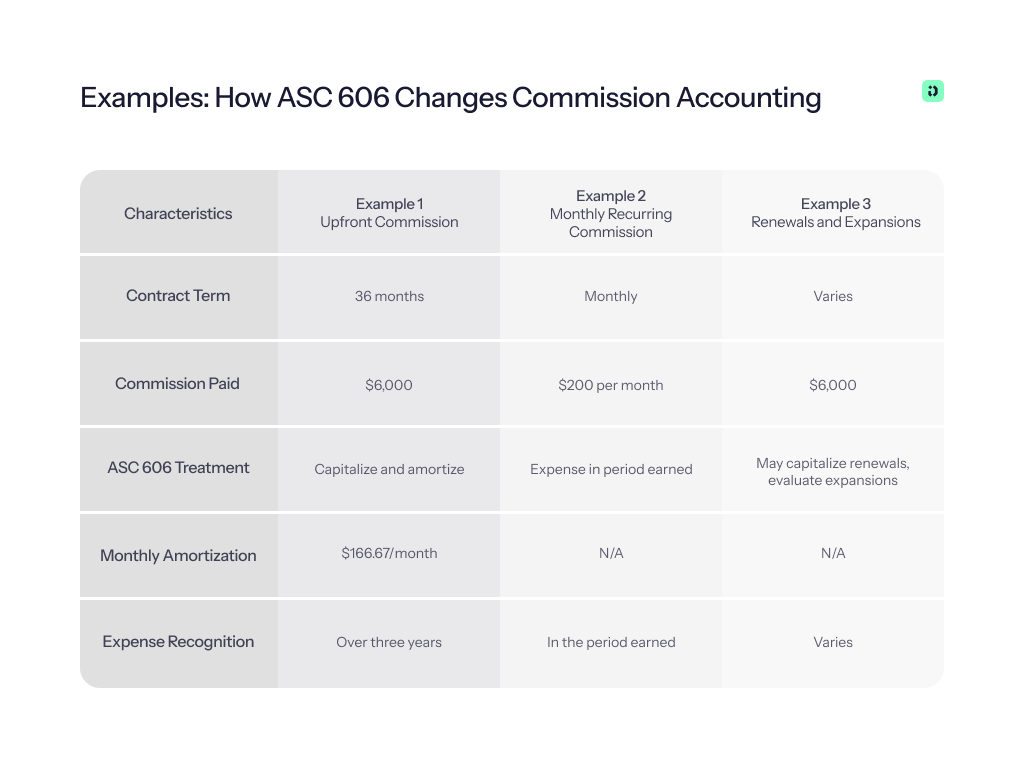

Examples: How ASC 606 Changes Commission Accounting

Let’s look at real world scenarios.

Example 1: Upfront Commission on a 3 Year SaaS Contract

Contract term: 36 months

Commission paid: $6,000

Under ASC 606: capitalize and amortize

Monthly amortization: $6,000 ÷ 36 = $166.67/month

Even if your sales rep receives $6,000 immediately, you recognize the expense over three years.

Example 2: Monthly Recurring Commissions

The sales rep is paid $200 per month based on monthly invoice collection.

No capitalization needed

Expense is recognized in the period the rep earns it

This is the simplest structure for ASC 606.

Example 3: Renewals and Expansions

Renewal commission may be capitalized, but only if it is incremental to securing the renewal.

Expansion commissions must be evaluated individually based on the new performance obligation.

ASC 606 requires careful documentation of the intent and purpose of each commission type.

Challenges Companies Face Under ASC 606

ASC 606 introduced major operational challenges:

1. Heavy Administrative Burden

Relying on manual spreadsheets makes ASC 606 compliance extremely time consuming and error-prone. As commission structures grow more complex, tracking amortization schedules, monitoring contract assets, and ensuring accurate period-by-period recognition become overwhelming. What starts as a simple tracking method quickly turns into a full-time administrative workload, leaving teams bogged down in data entry rather than focusing on strategic financial oversight.

2. Legacy Systems Aren’t Built for ASC 606

Older commission platforms and homegrown tools were never designed with ASC 606 requirements in mind. Because of this, they often lack essential capabilities such as capitalizing commissions, automating amortization over expected benefit periods, tracking ongoing contract assets, or handling churn and contract modifications accurately. Many organizations only discover these limitations after they’ve already run into compliance issues, realizing too late that their existing infrastructure cannot adequately support ASC 606 standards.

When compensation plans include multiple layers, variable components, or frequent adjustments, the accounting complexity increases significantly under ASC 606. Features like accelerators, bonuses, SPIFFs, and product-specific commission rates must all be evaluated to determine how and when related costs should be capitalized or expensed. Without a structured system in place, these intricate plans generate substantial workloads for finance teams and elevate the risk of misalignment with ASC 606 rules.

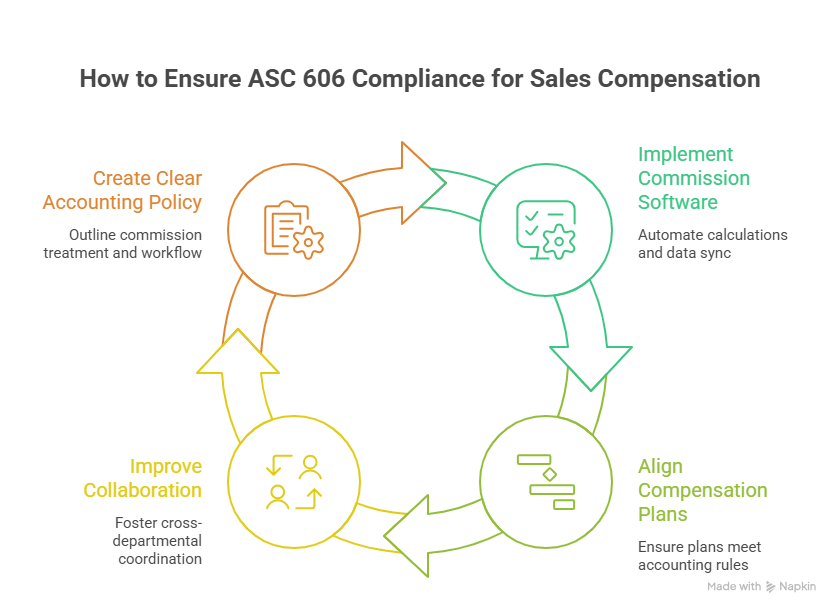

How to Ensure ASC 606 Compliance for Sales Compensation

Becoming compliant doesn’t need to be painful if you take the right steps.

1. Implement or Upgrade Commission Management Software

Look for tools that can:

Automate commission calculations

Capitalize and amortize commissions

Sync with CRM and ERP data

Create audit-ready documentation

Handle contract changes automatically

Automation reduces errors and saves hours, sometimes days, of manual work each month.

2. Align Compensation Plans with Accounting Rules

When designing plans, consider:

Contract length

Timing of payments

Whether commissions are tied to initial or ongoing performance

Incremental costs and justification

A streamlined plan often means easier compliance.

3. Improve Cross Department Collaboration

ASC 606 requires ongoing coordination between:

Finance

Sales Ops / RevOps

Legal

Sales leadership

Accounting

Establish recurring meetings and shared policies.

4. Create a Clear Commission Expense Accounting Policy

Your policy should outline:

Which commissions are capitalized

Amortization periods

Treatment of renewals

Adjustments for churn or contract changes

System workflow and review procedures

Consistency is key to compliance.

Best Practices Going Forward

To stay ASC 606 compliant and efficient:

Simplify commission plans whenever possible

Use automation to track amortization

Train sales and finance teams on ASC 606 requirements

Perform annual reviews of your compensation policy

Document everything; auditors expect clear rationale and reporting

ASC 606 compliance isn’t a one time project; it’s an ongoing discipline.

Conclusion

ASC 606 has reshaped the landscape of revenue recognition, but its impact extends far beyond finance. Sales compensation, once a straightforward operational process, now requires careful alignment with accounting principles and regulatory standards.

Understanding how ASC 606 affects commission recognition, documentation, and plan design is crucial for maintaining compliance, reducing risk, and creating transparency across your organization. Whether you’re a SaaS company with ongoing contracts or a service provider with complex incentives, adopting the right systems and policies will help you navigate these changes smoothly.

Frequently Asked Questions

What is ASC 606?

ASC 606 is a revenue recognition standard issued by the Financial Accounting Standards Board (FASB). It establishes a unified framework for how companies must recognize revenue from contracts with customers. Its purpose is to increase consistency and transparency in financial reporting across industries.

Why does ASC 606 matter for sales compensation?

ASC 606 impacts how companies treat the costs associated with earning revenue, including sales commissions. Under the standard, many commissions must be capitalized and amortized over the expected period of benefit rather than expensed immediately. This significantly changes how organizations account for and track compensation.

Do all sales commissions need to be capitalized under ASC 606?

Not always. Commissions directly tied to obtaining a contract typically need to be capitalized. However, some payments, such as those related to administrative tasks or non incremental activities, may still be expensed as incurred. Determining this requires careful analysis of your compensation structure.

How does ASC 606 affect commission payout timing?

ASC 606 doesn’t change when commissions are paid to sales reps; it changes how commissions are accounted for on the company’s financial statements. The payout process can remain the same, but the accounting treatment must align with capitalization and amortization requirements.

What types of commission plans are most impacted by ASC 606?

Plans with complexity, such as accelerators, bonuses, SPIFFs, ongoing deals, renewals, or product specific rates, are most affected. These structures often require detailed tracking to determine whether each component must be capitalized or expensed.

A SPIFF (Sales Performance Incentive Fund) is a short-term cash incentive tied to a specific, immediate action, usually selling a particular product, hitting a short-window target, or pushing a specific behavior the company wants right now.

SPIFFs are built for speed. They're announced, run for a defined stretch, usually days or weeks, and paid out fast, sometimes even same-day or same-week, specifically because the immediacy is what makes them effective. A SPIFF isn't meant to replace commission, it's meant to temporarily redirect a rep's attention toward something specific: clearing old inventory, pushing a new product launch, or closing out a slow month with extra motivation.

A draw in sales compensation is a guaranteed advance payment made to a salesperson against their future commissions. This means it is an advance against future commission, paid out on a regular schedule, usually monthly, so reps have predictable income before their pipeline turns into closed deals and actual commission.

Companies use draws to protect new reps' income during ramp. A brand-new AE with a three-month sales cycle isn't going to close anything in week two, but they still need to pay rent. A draw bridges that gap.

For sales professionals, understanding draw type matters because it affects real take-home pay, not just cash flow timing. Two reps can be offered the exact same dollar amount as a "draw" and end up with completely different financial outcomes, depending on which type it actually is.

Before comparing pay, it helps to be clear on what each role is actually on the hook for. They sit on the same team, but they're not doing the same job.

What Does an SDR Do?

SDRs own the top of the funnel. Their day is built around prospecting, outbound outreach, and lead qualification, all pointed at one outcome: booking meetings and creating a pipeline for AEs to work. SDRs generally aren't responsible for closing deals. Their job ends where the AE's job begins.

What Does an AE Do?

AEs own the deal once it's qualified. That means running discovery calls, delivering product demos, negotiating terms, and closing the deal. AEs carry direct revenue ownership, and in a lot of organizations, they also handle account management once the deal is signed. The pressure sits differently here: an AE's number is measured in dollars closed, not meetings booked.

%20(1).png)

.avif)